Updated

Does Smart Beta always outperform the index?

We expect Smart Beta to outperform over the long run, but it will not outperform every year.

Over the entire 53 year period analyzed in our backtest (from 1964 to 2016), Smart Beta outperformed the capitalization-weighted index.

Specifically, the modified index used by Smart Beta beat the benchmark by 0.82% per year before taxes, when implemented using the 500 largest securities by market capitalization, and 0.98% per year, when implemented using the 1000 largest securities. This was all done without affecting the overall risk (volatility) of the portfolio.

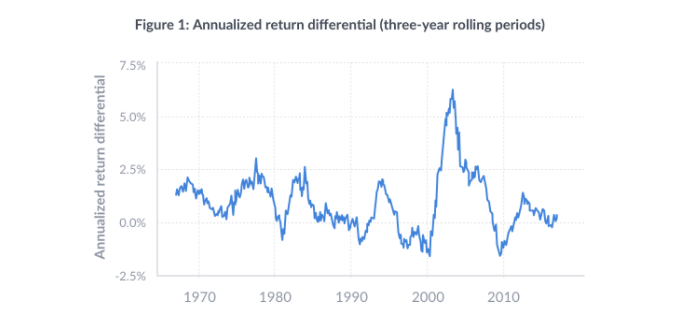

Although the modified index outperformed in over three quarters of the three-year periods, it is important to note that there have been three-year periods in which the annual underperformance equaled almost 2% per year. The figure below displays the amount by which the modified index has outperformed (positive values) or underperformed (negative values) the cap-weighted benchmark over rolling three-year periods.

Annualized return differential between the Modified Index and the Market Capitalization Weighted Index (three-year rolling periods; CRSP Top 500)

For more details, see our Smart Beta White Paper.

Assumptions

This figure is a historical return based on backtesting. and did not rely on actual trading using client assets. Backtested results are hypothetical and not an indicator of any investor’s actual current or future experience and is provided for illustrative purposes only. Hypothetical performance is developed by the retroactive application of a model designed with the benefit of hindsight and has inherent limitations. Specifically, hypothetical results do not reflect actual trading or the effect of material economic and market factors on the decision-making process. Wealthfront assumed we would have been able to purchase the securities recommended by the model and the markets were sufficiently liquid to permit all trading. We also assumed that an investor’s risk score and target allocation would not have changed during the time period shown; however, actual investors may have experienced changes to their allocation plan in response to changing suitability profiles and investment objectives. Furthermore, material economic and market factors that might have occurred during the time period could have had an impact on decision-making. Investors evaluating this information should carefully consider the processes, data, and assumptions used by Wealthfront in creating its simulations which are described above. Backtested results were adjusted to reflect the reinvestment of dividends and other earnings.

This communication has been prepared solely for informational purposes only. Nothing in this communication should be construed as an offer, recommendation, or solicitation to buy or sell any security or a financial product. Any links provided to other server sites are offered as a matter of convenience and are not intended to imply that Wealthfront or its affiliates endorses, sponsors, promotes and/or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Wealthfront offers a free software-based financial advice engine that delivers automated financial planning tools to help users achieve better outcomes. Investment management and advisory services are provided by Wealthfront Advisers LLC, an SEC registered investment adviser, and brokerage related products are provided by Wealthfront Brokerage LLC, a member of FINRA/SIPC.

Wealthfront, Wealthfront Advisers and Wealthfront Brokerage are wholly owned subsidiaries of Wealthfront Corporation.

© 2025 Wealthfront Corporation. All rights reserved.

When Wealthfront replaces investments with “similar” investments as part of the tax-loss harvesting strategy, it is a reference to investments that are expected, but are not guaranteed, to perform similarly and that might lower an investor’s tax bill while maintaining a similar expected risk and return on the investor’s portfolio. Wealthfront assumes no responsibility to any investor for the tax consequences of any transaction.

Tax loss harvesting may generate a higher number of trades due to attempts to capture losses. There is a chance that Wealthfront trading attributed to tax loss harvesting may create capital gains and wash sales and could be subject to higher transaction costs and market impacts. In addition, tax loss harvesting strategies may produce losses, which may not be offset by sufficient gains in the account and may be limited to a $3,000 deduction against income. The utilization of losses harvested through the strategy will depend upon the recognition of capital gains in the same or a future tax period, and in addition may be subject to limitations under applicable tax laws, e.g., if there are insufficient realized gains in the tax period, the use of harvested losses may be limited to a $3,000 deduction against income and distributions. Losses harvested through the strategy that are not utilized in the tax period when recognized (e.g., because of insufficient capital gains and/or significant capital loss carryforwards), generally may be carried forward to offset future capital gains, if any.

Wealthfront’s investment strategies, including portfolio rebalancing and tax loss harvesting, can lead to high levels of trading. High levels of trading could result in (a) bid-ask spread expense; (b) trade executions that may occur at prices beyond the bid ask spread (if quantity demanded exceeds quantity available at the bid or ask); (c) trading that may adversely move prices, such that subsequent transactions occur at worse prices; (d) trading that may disqualify some dividends from qualified dividend treatment; (e) unfulfilled orders or portfolio drift, in the event that markets are disorderly or trading halts altogether; and (f) unforeseen trading errors. The performance of the new securities purchased through the tax-loss harvesting service may be better or worse than the performance of the securities that are sold for tax-loss harvesting purposes.

Wealthfront only monitors for tax-loss harvesting for accounts within Wealthfront. The client is responsible for monitoring their and their spouse's accounts outside of Wealthfront to ensure that transactions in the same security or a substantially similar security do not create a “wash sale.” A wash sale is the sale at a loss and purchase of the same security or substantially similar security within 30 days of each other. If a wash sale transaction occurs, the IRS may disallow or defer the loss for current tax reporting purposes. More specifically, the wash sale period for any sale at a loss consists of 61 calendar days: the day of the sale, the 30 days before the sale, and the 30 days after the sale. The wash sale rule postpones losses on a sale, if replacement shares are bought around the same time.

The effectiveness of the tax-loss harvesting strategy to reduce the tax liability of the client will depend on the client’s entire tax and investment profile, including purchases and dispositions in a client’s (or client’s spouse’s) accounts outside of Wealthfront and type of investments (e.g., taxable or nontaxable) or holding period (e.g., short- term or long-term). Except as set forth below, Wealthfront will monitor only a client’s (or client’s spouse’s) Wealthfront accounts to determine if there are unrealized losses for purposes of determining whether to harvest such losses. Transactions outside of Wealthfront accounts may affect whether a loss is successfully harvested and, if so, whether that loss is usable by the client in the most efficient manner.

A client may also request that Wealthfront monitor the client’s spouse’s accounts or their IRA accounts at Wealthfront to avoid the wash sale disallowance rule. A client may request spousal monitoring online or by calling Wealthfront at 844-995-8437. If Wealthfront is monitoring multiple accounts to avoid the wash sale disallowance rule, the first taxable account to trade a security will block the other account(s) from trading in that same security for 30 days.

Comments are moderated prior to publication